Updated: January 2026

Use Section 179 to expense qualifying business equipment and software in the year it’s placed in service. This guide covers the 2026 rules (tax years beginning in 2026), including current dollar limits, phase-outs, vehicle caps, and how Section 179 can be combined with bonus depreciation.

Quick Reference: 2026 Section 179 Limits

Max Deduction (2026):

$2,560,000 (phase-out begins above $4,090,000)

Bonus Depreciation :

100% (applies after Section 179)

New & Used Equipment:

Qualifies for full Section 179 deduction

Specialized (Non‐Passenger) Vehicles:

Qualifies for full Section 179 deduction

Certain SUVs (6,000–14,000 lbs GVWR):

$32,000 max first-year Section 179; remainder depreciated

Business‐Use Requirement:

>50% business use; deduction limited to % of business use

Note: The Section 179 deduction phases out dollar-for-dollar when the total cost of qualifying property placed in service exceeds $4,090,000 and is fully phased out at $6,650,000.

These limits are updated annually for inflation. For background on recent rule changes and effective dates, see our Legislative History page.

What Is Section 179 (and Why Does It Matter in 2026)?

Section 179 of the Internal Revenue Code empowers businesses to deduct the full purchase price of qualifying equipment and software in the same tax year they’re put into service. Instead of stretching depreciation across several years, you can claim the entire cost upfront—dramatically improving your cash flow and creating immediate tax benefits.

Why Section 179 Matters for Your Business

- Immediate Tax Impact: Rather than waiting years for depreciation benefits, claim the deduction in 2026

- Enhanced Cash Flow: Keep more working capital in your business when you need it most

- Strategic Growth: Upgrade equipment sooner and maintain competitive advantages in your market

How the 2026 Deduction Limits and Phase‐Out Threshold Work

What Is the Maximum Section 179 Deduction for 2026?

For tax years beginning in 2026, businesses can elect to expense up to $2,560,000 of qualifying purchases. This is the maximum total Section 179 amount you can write off, subject to the taxable income limitation and the phase-out rules below.

- Placed in service during the tax year you’re claiming the deduction

- Used for business purposes more than 50% of the time

- Qualifies under IRS guidelines

Spending Cap and Phase-Out Rules

The Section 179 deduction begins to phase out when the total cost of qualifying property placed in service exceeds $4,090,000:

- Phase-out begins: above $4,090,000 of total qualifying property placed in service

- Dollar-for-dollar reduction: the $2,560,000 limit is reduced by the amount over $4,090,000

- Fully phased out: at $6,650,000

- After Section 179: remaining basis may still qualify for bonus depreciation (if eligible)

How Does Section 179 Apply to Business Vehicles?

Special rules apply to vehicles:

- Vehicles rated at 6,000 lbs. GVWR or less follow standard depreciation rules

- SUVs over 6,000 lbs. GVWR but under 14,000 lbs. GVWR: Limited to $32,000 Section 179 deduction for certain SUVs

- Vehicles over 6,000 lbs. GVWR such as heavy work trucks and vans may be eligible for full Section 179 expensing

- Vehicles with beds at least six feet long are not subject to the SUV limitation

Learn more about Section 179 Vehicle Deductions

How Do Carryover & Limitations Work?

Your Section 179 deduction cannot exceed your business’s net taxable income. However, if your Section 179 election exceeds your taxable business income in a given year, you can choose a partial Section 179 election. Any unused portion of the deduction carries forward to subsequent tax years, allowing you to apply it once you have sufficient income. This means if you can’t fully utilize Section 179 in the current year, you retain the remaining deduction for future use—ensuring you never lose the benefit.

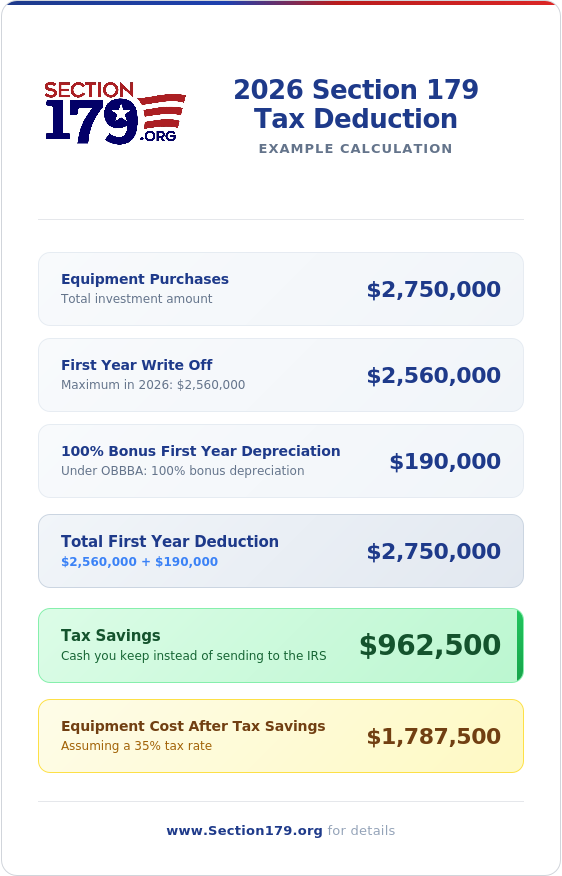

Example: How Does Section 179 Generate Tax Savings?

This simplified example illustrates how Section 179 can reduce after-tax equipment costs. It assumes the purchase qualifies, the business has enough taxable income to use the full Section 179 election, and any remaining basis is eligible for bonus depreciation. For a $2,750,000 purchase:

- Section 179 Deduction: $2,560,000

- Bonus Depreciation: $190,000 (if eligible)

- Total Tax Savings: $962,500 (assumes a 35% combined tax rate)

- Final Equipment Cost: $1,787,500

Which Assets Qualify for Section 179 in 2026?

Common Eligible Assets

- Manufacturing equipment and machinery

- Business vehicles

- Computers and office technology

- Off-the-shelf software

- Office furniture and equipment

- Certain building improvements

See the full Section 179 qualifying property rules and examples.

What Are the Requirements for Qualifying Property?

- Must be primarily for business use (>50%)

- New or used equipment qualifies

- Must be placed in service by the end of your tax year (December 31, 2026 for calendar-year taxpayers)

- Cannot be inherited or gifted property

How to Plan Your Section 179 Strategy

What Is Section 179 Qualified Financing?

Take advantage of specialized Section 179 Qualified Financing to maximize your tax benefits while preserving working capital:

- Minimal down payments with flexible terms aligned to your cash flow

- Claim full Section 179 deduction even on financed equipment

- Tax savings often exceed your first-year payments

- Quick approvals to help meet year-end placed-in-service deadlines

- Financing structures designed specifically for Section 179-eligible purchases

Many equipment vendors offer Section 179 Qualified Financing packages specifically designed for Section 179‐eligible purchases:

- Extended payment terms

- Seasonal payment schedules

- Deferred payment options

- Equipment delivery guarantees before year-end

How Does Section 179 Compare to Bonus Depreciation in 2026?

- Section 179: $2,560,000 maximum (tax years beginning in 2026) with a taxable income limitation and phase-out rules

- Bonus Depreciation: generally 100% for qualified property acquired and placed in service after Jan. 19, 2025

- Common approach: use Section 179 first, then apply bonus depreciation to any remaining eligible basis

What Records Are Needed for a Section 179 Claim?

Maintain thorough records including:

- Purchase invoices and contracts

- Proof of payment

- Installation or in-service dates

- Business usage logs

- Form 4562 filing documentation

How Do State Tax Laws Affect Section 179 in 2026?

Federal Section 179 rules apply nationwide, but state conformity varies—some states match federal treatment while others limit or decouple from Section 179 and/or bonus depreciation. Confirm current state rules with your tax professional.

How Do I Make the Section 179 Election in 2026?

File Form 4562 with your tax return. For a step-by-step walkthrough, see How to Apply (Section 179 Election):

- List qualifying property

- Specify amount to expense

- Include business-use percentage

- Document vehicle information if applicable

What Are Expert Tips for Maximizing Section 179 in 2026?

- Plan Major Purchases Around Tax Years: Time your acquisitions to maximize immediate write‐offs.

- Track Business Usage Carefully: Logging usage is crucial for vehicles and other assets.

- Consider State Tax Implications: Different states may have unique limits or rules.

- Maintain Detailed Records: Keep documentation for five+ years in case of audit.

- Review Annually with a Tax Professional: Tax laws can shift year to year; stay current.

What Are My Next Steps?

- Use our 2026 Section 179 Calculator – Estimate potential first-year deductions and tax savings.

- Review our Section 179 FAQs Section – Find quick answers to common Section 179 questions.

- Consult Tax Professionals – Get tailored advice for your specific situation.

Where Can I Find Additional Resources?

- Section 179 FAQs

- Bonus Depreciation Guide

- State Conformity Rules

Disclaimer: This guide provides general information about Section 179 and is not tax advice. Always consult qualified tax professionals regarding your specific circumstances.

Sources: Rev. Proc. 2025-32 (2026 inflation adjustments); IRS Notice 2026-11 (bonus depreciation guidance); Instructions for Form 4562.